- by admin

- Comment Off

- 251 views

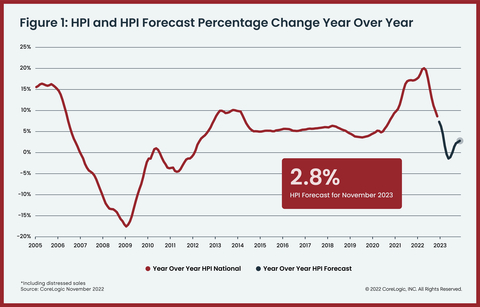

Knock Buyer-Seller Market Index shows that buyers will have more leverage in the West, while sellers will maintain an advantage in the East As the reality of high home prices and higher mortgage rates sets in, U.S. homebuyers will gain some leverage in 2023. However, shoppers are in for very different experiences depending on where in the U.S. they are looking to move, according to the Knock Buyer-Seller Market Index 2023 forecast, which shows a clear divide between the best markets for buyers versus sellers. According to the Index, which analyzes key housing market metrics to measure the degree to which the nation’s 100 largest markets favor home buyers or sellers, the top 5 buyers’ markets are west of the Mississippi, while the top 5 sellers’ markets are concentrated in the East Coast. “With home prices and interest rates cutting into purchasing power, the relocation hotspots where prices grew quickly during the pandemic will increasingly favor buyers in 2023, while more mid-sized markets offering good job opportunities and affordable housing will be the top performing real estate markets in 2023,” said Knock Co-Founder and CEO Sean Black. “This will usher in a more balanced housing market. However, home shoppers will find different scenarios depending where in the U.S. they are looking.” In like a lion, out like a lamb As 2022 came to a close it was clear the combination of high home prices and interest rates put an end to the frenetic pandemic housing market. Based on the November 2022 Buyer-Seller Index, the latest month of available data, inventory rose in 80 of the 100 largest housing markets and all but two moved at least marginally toward favoring buyers. A total of 2,336,520 homes were sold in the 100 largest housing markets in the first 11 months of 2022, down 19% from a year earlier. Median days on market increased to 22, up from 13 in November 2021. The average sale-to-list ratio, which measures how close homes are selling to their asking price, was 98%, down from 99% in October and 100% a year ago. There were 14 buyers’ markets in November 2022, 46 markets favored sellers and 40 were in neutral territory. Hot pandemic markets become 2023 top buyers’ markets This year’s top buyers’ markets are all west of the Mississippi and were popular relocation spots during the pandemic, which caused home prices to accelerate at a faster pace than the rest of the nation on average. Prices in the top five buyers’ markets rose by 44.6% on average between January 2020 and last month, compared to 34.9% for the rest of the nation during the same period. In rank order, the top 5 buyers’ metros for 2023 are Phoenix-Mesa-Chandler, Ariz.; Colorado Springs, Colo.; Las Vegas-Henderson-Paradise, Nev.; Dallas-Fort Worth-Arlington, Texas and Denver-Aurora-Lakewood, Colo. Although these markets will see median home price growth moderate and even decline from their pandemic peaks in 2023, prices are forecast to end the year 38% above pre-pandemic levels, 3% higher than the national average change. A sign of a slowing market, inventory is expected to grow significantly (54.4% on average) in the top buyers’ markets. Denver will see inventory grow by nearly 100%, ranking second behind Charlotte, N.C., which is projected to lead the nation in inventory growth at 148.3%. Sellers will have the advantage in smaller, more affordable markets Concentrated in the East Coast, the top sellers’ markets are forecast to see the strongest growth in home sales and listing prices in 2023. They tend to be smaller to mid-size markets with populations under 1 million, where home prices remain affordable. Despite increasing by as much as 50% since January 2020, prices in the top sellers’ markets remain well below the national median home price of $374,000. Fayetteville, N.C.; Harrisburg-Carlisle, Pa.; Syracuse, N.Y.; Hartford-East Hartford-Middletown, Conn. and York-Hanover, Pa., top the list of Knock’s best markets for sellers in 2023. Home sales across the top sellers’ markets are forecast to rise by between 5% and 18% over the next 12 months. The exception is Hartford, Conn., where home sales are projected to dip by 1.7%. In contrast, sales are forecast to decline by 16.3% for the rest of the nation by the end of 2023. On average, the median home price in these markets is expected to increase 8.3%, compared to the less than 1% increase forecast for the U.S. as a whole. Days on market will average 15 days, half the forecasted national median of 30 days, while average months’ supply will be just one month, compared to 3.1 months for the 100 largest markets. Housing market will gain momentum in the spring before turning to buyers According to the Index, the nation’s 100 largest housing markets will continue to teeter in neutral territory over the next few months, gain some momentum toward sellers in the spring and then move firmly into buyers’ market territory by summer – a trend that will continue through the end of the year. By November 2023, 36 markets are forecast to be buyers’ markets (up from 14 in November 2022), 41 markets will remain sellers’ markets (down from 46), and 23 will be neutral. As the market continues to cool, the 100 largest markets are projected to see home sales decline by 16.3% year over year. Fayetteville, Ark., will face the largest falloff at -22.9%. By the middle of 2023, months’ supply will surpass three months for the first time since the summer of 2019. Charlotte, N.C., is forecast to lead the nation in months’ supply at 12.7 – double that of Port St. Lucie, Fla., which is forecast to have the second-highest months’ supply at 6.2. Nationally, the median sales price is forecast to peak in June at $386,000, consistent with a typical home selling season. By November, the median price is forecast to be $374,000, basically flat compared to November 2022. Median days on market will continue to rise throughout 2023, reaching 30 days across the U.S. by November 2023, with Colorado Springs, Colo., leading the nation at 121 days. Average sale prices across large housing markets are forecast to remain lower than the average ask price in each of the next 12 months, keeping the sale-to-list ratio below 100% through 2023.

Read More